Option pricing models

Negative prices

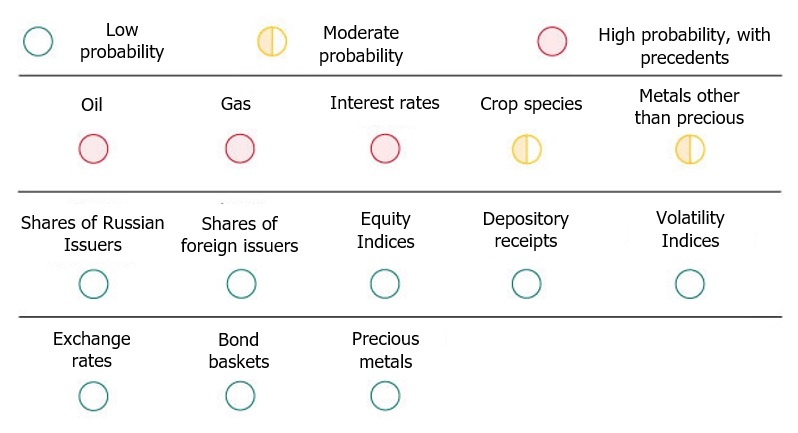

The probability of futures prices turning negative is high for interest rates and certain commodities, such as oil, gas, and metals. For assets in these groups, negative prices are either already allowed or may be allowed at some time in the future.

Information about option pricing model used for each underlying asset is available at the website of NCC in the Derivatives Market Risk Management section.

Probability of negative prices for different underlying assets

Option pricing models

The MOEX Derivatives Market risk management currently supports the following option pricing models:

- The Black model

- The Bachelier model

Detailed information on the option pricing models applicable is available in the Methodology for Calculating the Theoretical Option Price.

The main difference between the Black and Bachelier models lies in the theoretical distribution of the futures price. For this reason, the Black model only applies when futures prices are positive, while the Bachelier model is used when the prices are low positive or negative.

| The Black model | The Bachelier model | |

|---|---|---|

| Theoretical futures price distribution | Log+normal | Normal |

| Volatility measurement unit | %, YoY | Futures contract point, YoY |

| Applicable with low positive or negative futures prices | No | Yes |

| Applicable with high positive or futures prices | Yes | No |

Switch between option pricing models

Information about option pricing model used to each underlying assets is available at the website of NCC in the Derivatives Market Risk Management section.

By default, the Black model is used for all underlying assets. The switch to the Bachelier model occurs when negative futures prices are highly possible.

In order to measure the likelihood of negative prices, NCC introduces three monitoring zones for the settlement price of the first futures (F) determined through intraday or evening clearing. Monitoring zones are based on MinPrice (underlying asset's minimal price) used in the initial market calculation.

Monitoring zones

| Green zone | Yellow zone | Red zone | |

|---|---|---|---|

| Zone range | F ≥ 1.5 х MinPrice |

F < 1.5 х MinPrice F ≥ MinPrice |

F < MinPrice |

| Option pricing model applied | The Black model |

The Black model (by

default) or the Bachelier model by NCC's decision |

The Bachelier model |

MinPrice values for underlying assets are available at the website of NCC in the Derivatives Market Risk Management section.

Should the option pricing model be changed to the Bachelier model, the switch back to the Black model is decided by the NCC.