What is an option?

An option is a contract giving the buyer the right to buy or sell an underlying asset at a specific price in the future, with a counter obligation imposed on the seller.

The main difference between options and futures is precisely that the holder of an option has the right, not the obligation, to buy/sell the underlying asset. In a futures transaction, an obligation arises for both parties to the contract.

The main difference between options and futures is precisely that the holder of an option has the right, not the obligation, to buy/sell the underlying asset. In a futures transaction, an obligation arises for both parties to the contract.

A few basic terms

The price of the underlying asset at which a trade under an option will take place in the future is called the strike price.

A call option — is a type of option that gives the buyer the right to buy the underlying asset at a predetermined price on a specified date, with the seller of such option undertaking to sell the underlying asset.

A put option — is a type of option that gives the buyer the right to sell the underlying asset at a predetermined price on a specified date, with the seller of such an option undertaking to buy the underlying asset.

Expiration — is the termination of trading in a derivative contract (option or futures) on an exchange.

A call option — is a type of option that gives the buyer the right to buy the underlying asset at a predetermined price on a specified date, with the seller of such option undertaking to sell the underlying asset.

A put option — is a type of option that gives the buyer the right to sell the underlying asset at a predetermined price on a specified date, with the seller of such an option undertaking to buy the underlying asset.

Expiration — is the termination of trading in a derivative contract (option or futures) on an exchange.

What is the price of an option?

Since the buyer and the seller are on unequal terms (the former has the right and the latter the obligation) and bear different risks, the buyer will have to pay the seller a

premium.

The premium is the price for the risk accepted by the seller as it cannot decline to exercise the option and its losses are potentially unlimited. By contrast, the option buyer only risks losing the premium paid and can decline to exercise if the market goes against its position.

The premium varies depending in the type of an option (call or put) and strike price. Mathematically, it is derived from a complex model with several variables and is called the theoretical value of an option. It can serve as a rough guide for the trading member. In practice, the premium is what is traded on the order book. There is a separate order book for each strike price and option type.

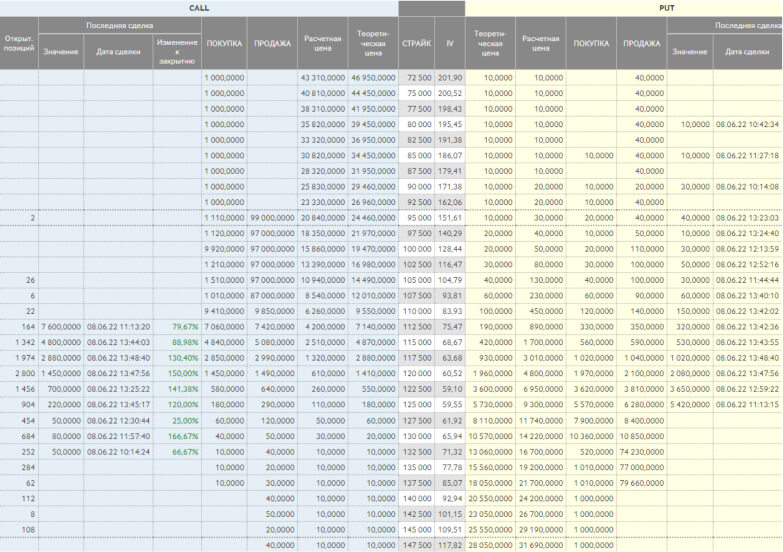

An options board — is a special summary table showing the market data for options on the same underlying asset with one expiration date.

The Moscow Exchange website has the Options Chain page where you can select the underlying asset and view bids/offers, recent transaction data, open interest, estimated and theoretical prices for each strike price of call and put options.

The premium is the price for the risk accepted by the seller as it cannot decline to exercise the option and its losses are potentially unlimited. By contrast, the option buyer only risks losing the premium paid and can decline to exercise if the market goes against its position.

The premium varies depending in the type of an option (call or put) and strike price. Mathematically, it is derived from a complex model with several variables and is called the theoretical value of an option. It can serve as a rough guide for the trading member. In practice, the premium is what is traded on the order book. There is a separate order book for each strike price and option type.

An options board — is a special summary table showing the market data for options on the same underlying asset with one expiration date.

The Moscow Exchange website has the Options Chain page where you can select the underlying asset and view bids/offers, recent transaction data, open interest, estimated and theoretical prices for each strike price of call and put options.

Open of the option chain for options on the RTS-9.22 futures with an expiration date of 23 June 2022

What is the underlying asset of an option?

An option is a derivative financial instrument, so its price depends on the price of the underlying asset.

The underlying assets can come in a variety of forms:

The underlying assets can come in a variety of forms:

Financial instruments (shares, bonds)

Currency

Indices

Commodities (metals, oil, agricultural products, etc.)

Interest rates

Other derivative financial instruments (futures)

What kinds of options exist?

Options can be classified according to several criteria:

1. Cash-settled and physically deliverable

When an option is bought, the underlying asset does not necessarily have to be delivered, as some options are settled in cash. When a cash-settled option is exercised, the underlying asset is not delivered; instead, if the option turns out to be in the money, the cash is transferred to the buyer. Any kind of asset can be used as the underlying for cash-settled options.

Deliverable options involve the delivery of underlying assets, which can be securities, futures or commodities.

Deliverable options involve the delivery of underlying assets, which can be securities, futures or commodities.

2. Equity-style and futures-style options

Equity-style and futures-style options differ in how the premium is paid. The former involves a one-time payment of the premium when the option is purchased, in which case the position is not market-to-market until the option is exercised and no variation margin is required. Initial margin (IM) is only locked in with the seller of the option against the performance obligation.

The buyer of a futures-style option does not pay the premium to the seller. Payment of the premium is "spread over time" through daily transfers of variation margin until the contract expires, with the IM locked in both the seller and the buyer of the option.

The buyer of a futures-style option does not pay the premium to the seller. Payment of the premium is "spread over time" through daily transfers of variation margin until the contract expires, with the IM locked in both the seller and the buyer of the option.

A few important terms

Initial Margin (IM) is the amount of money that is blocked on the brokerage account when a position in a derivative contract is opened. IM is a part of the nominal value of the contract in roubles. Its amount is determined by the risk rate, which is set by NCC for each contract depending on the risk of the underlying asset. IM may change until the exercise of the contract. If the size of initial margin increases and there are no funds available on the account, the broker may mandatorily close out the client's positions.

Variation Margin – is the profit or loss running on an open position since the last clearing or since the opening of the position if there has been no clearing yet. Variation margin is fixed, and funds are deposited/withdrawn from the account at each clearing cycle. After clearing ends, the next trading session starts, and the variation margin is calculated again.

Variation Margin – is the profit or loss running on an open position since the last clearing or since the opening of the position if there has been no clearing yet. Variation margin is fixed, and funds are deposited/withdrawn from the account at each clearing cycle. After clearing ends, the next trading session starts, and the variation margin is calculated again.

3. European and American style options

American style options can be exercised early, i.e. at any time prior to expiration. European style options can be exercised only at expiration.

For example, an American style option exercisable on 17 March can be exercised on 17 March or any day earlier, e.g. 15 March, whereas a European style option with the same exercise date can only be exercised on 17 March.

For example, an American style option exercisable on 17 March can be exercised on 17 March or any day earlier, e.g. 15 March, whereas a European style option with the same exercise date can only be exercised on 17 March.

What is the market value of an option?

The option market value — is the premium that is determined in the market and paid to the seller of the contract. It is made up of two parts:

- Intrinsic value;

- Time value.

Intrinsic value of an option is the income that the option buyer receives when the option is exercised (excluding the premium paid). It cannot be negative and depends on the difference between the market price of the underlying asset and the strike.

The intrinsic value of call options is greater than zero when the price of the underlying asset is greater than the strike price. It equals the difference between the price of the underlying asset and the strike.

On the contrary, the intrinsic value of put options is greater than zero when the price of the underlying asset is lower than the strike price. It equals the difference between the strike and the price of the underlying asset.

Depending on where the price of the underlying asset (UA) lies in relation to the strike price, options may vary as follows:

On the contrary, the intrinsic value of put options is greater than zero when the price of the underlying asset is lower than the strike price. It equals the difference between the strike and the price of the underlying asset.

Depending on where the price of the underlying asset (UA) lies in relation to the strike price, options may vary as follows:

- An option is "out of the money" ("OTM") options when it has zero intrinsic value

- An option is "at the money" ("ATM") when the price of the UA equals the strike price

- "In the money" ("ITM") means the intrinsic value greater than zero.

Time value refers to the portion of an option's premium that is attributable to the amount of time remaining until the expiration of the option contract. Time value intuitively can be understood as the probability that an option becomes profitable in the future.

Time value = Market value - Intrinsic value

The value of 'out of the money' options is equal to the time value, while "in the money" options has a minimal share of the time value because they have a high intrinsic value.

As we get closer to expiration, the time value gradually decreases because there is less and less time left for the option to become profitable. At expiration, the value of the option equals its intrinsic value and the time component becomes zero.

Time value = Market value - Intrinsic value

The value of 'out of the money' options is equal to the time value, while "in the money" options has a minimal share of the time value because they have a high intrinsic value.

As we get closer to expiration, the time value gradually decreases because there is less and less time left for the option to become profitable. At expiration, the value of the option equals its intrinsic value and the time component becomes zero.

Factors that determine the option value

The value of options is affected by many factors, with put and call options being affected in different directions. We have compiled the most important factors into the table below. It is worth mentioning that the effect of a particular factor should be considered with other things being equal, because in reality the value of options can be affected by several values at the same time.

Factor

Direction

Call price

Put price

Explanation

Underlying asset (UA) price

The higher the value of the UA, the more likely it is that the call option will be in the money and the put option will not.

Strike

The higher the strike, the lower the probability that it will be reached on a call option. Conversely, the probability of breaking the strike increases for put options.

Volatility

When volatility is high, the probability of reaching a strike increases for both types of options.

Time to expiration

The shorter the time to expiration, the less likely it is that the option will be profitable.

Dividend

Paying dividends on a stock reduces its value and the value of call options but has a positive effect on the price of put options.

Risk-free

rate

rate

An increase in the risk-free rate leads to an increase in the price of call options and a decrease in the price of put options.

Why trade options?

Options are used for different purposes:

- Profit from changes in the price of the underlying asset. Since the profit on an option depends on the price of the underlying asset, it is possible to benefit from its rise or fall without having to deal directly with it. More on this in the section "How much profit or loss can I make from options?".

- To hedge price risk. Buying an option is similar to buying insurance. If an investor anticipates that the value of the underlying asset will rise in the future and wants to protect itself against buying at an unfavourable price, he/she can buy a call option, fixing the purchase price of the underlying asset. Conversely, to avoid selling the underlying too cheaply in the future, he/she can hedge buying a put option. More information on this in the section "Hedging with options".

- Profit from option premium. Selling an option, on the contrary, is like selling insurance. The option seller receives a premium for assuming the risk that the price will move in the direction of the buyer's position. Nevertheless, for the buyer to make a profit, the price of the underlying asset not only broke through the strike, but also reached the point at which the buyer's profit covers the premium paid (the breakeven point). You can also read about this in the section "How much profit or loss can I make from options?".

- Building an options strategy. Mostly, more than one option with different characteristics is used to trade option strategies. This allows creating different profit/loss ratios and benefit from more complex market movements. More information on this in the section "Option strategies".

How much profit or loss can I make from options?

The easiest way to understand how a profit or loss on options is to use charts. In Examples 1 and 2, the charts show the profit or loss that would be made if the option were exercised now. Here, the horizontal axis plots the price of the underlying asset at the time the option is exercised, so there is no time value.

As shown in the charts, buyers of options risk only the premium paid, while sellers' losses are potentially unlimited.

Buyers of call options expect the value of the underlying to be greater than the strike plus the premium (breakeven point), while sellers anticipate that it will not rise to this level.

Buyers of put options expect the price of the underlying to be below the strike minus the premium (breakeven point), while sellers expect the price not to fall below this level.

As shown in the charts, buyers of options risk only the premium paid, while sellers' losses are potentially unlimited.

Buyers of call options expect the value of the underlying to be greater than the strike plus the premium (breakeven point), while sellers anticipate that it will not rise to this level.

Buyers of put options expect the price of the underlying to be below the strike minus the premium (breakeven point), while sellers expect the price not to fall below this level.

Example 1. A call option with a strike of 100 and a premium of 5

Example 2. A put option with a strike of 50 and a premium of 5

Examples 3 and 4 show the profit/loss of the parties to an option based on its time value, i.e. the horizontal axis plots the price of the underlying asset not at the time of exercise, but some time before. Thus, the time value increases the profit of the buyer and consequently reduces the profit of the option seller.

Example 3. A call option with a strike of 100 and a premium of 5

Example 4. A put option with a strike of 50 and a premium of 5

Hedging with options

Options can be used to hedge the risk that the price of an underlying asset will rise or fall in the future. Let's look at examples of how this happens.

Example 1. Hedging the buyer"s risk

Buying a call option allows hedging the buyer's risk in the market the underlying asset is traded. The buyer's risk is to buy the asset at a too high price.

Suppose the underlying asset is currently worth 100. An investor who wants to buy it in three months buys a call option with strike = 100, premium = 5 and exercisable in three months.

Possible scenarios in 3 months:

1. The price of the underlying asset has risen to 110

In this case, the investor exercises the option, i.e. buys the underlying asset for 100. Its profit* is equal to the option profit minus the premium paid = (110 - 100) - 5 = 5

2. The price of the underlying asset has fallen to 90

In this case, it is not profitable to exercise the option, so it remains unexercised, and the investor buys the underlying asset for 90 in the spot. Its profit* equals the savings from buying the underlying asset minus the premium paid = (100 - 90) - 5 = 5

So, if the price moves up or down equally, the buyer of the underlying gets the same result thank to buying a call option.

Suppose the underlying asset is currently worth 100. An investor who wants to buy it in three months buys a call option with strike = 100, premium = 5 and exercisable in three months.

Possible scenarios in 3 months:

1. The price of the underlying asset has risen to 110

In this case, the investor exercises the option, i.e. buys the underlying asset for 100. Its profit* is equal to the option profit minus the premium paid = (110 - 100) - 5 = 5

2. The price of the underlying asset has fallen to 90

In this case, it is not profitable to exercise the option, so it remains unexercised, and the investor buys the underlying asset for 90 in the spot. Its profit* equals the savings from buying the underlying asset minus the premium paid = (100 - 90) - 5 = 5

So, if the price moves up or down equally, the buyer of the underlying gets the same result thank to buying a call option.

Example 2. Hedging the seller"s risk

Buying a put option allows hedging the seller's risk in the spot market. The seller's risk is to sell the asset too cheaply.

Suppose the underlying asset is currently worth 50. An investor who wants to sell it in three months buys a put option with strike = 50, premium = 5 and exercisable in three months.

Possible scenarios in 3 months:

3. The price of the underlying asset has fallen to 40

In this case, the investor exercises the option, i.e. sells the underlying asset for 50. Its profit* is equal to the option profit minus the premium paid = (50 - 40) - 5 = 5

4. The price of the underlying asset rose to 60

In this case, it is not profitable to exercise the option, so it remains unexercised and the investor sells the underlying asset for 60 in the spot market. Its profit* equals the gain on the sale of the underlying asset minus the premium paid = (60 - 50) - 5 = 5

So, if the price moves up or down equally, the seller of the underlying gets the same result thank to buying a put option.

* Profit excluding time value of money

Suppose the underlying asset is currently worth 50. An investor who wants to sell it in three months buys a put option with strike = 50, premium = 5 and exercisable in three months.

Possible scenarios in 3 months:

3. The price of the underlying asset has fallen to 40

In this case, the investor exercises the option, i.e. sells the underlying asset for 50. Its profit* is equal to the option profit minus the premium paid = (50 - 40) - 5 = 5

4. The price of the underlying asset rose to 60

In this case, it is not profitable to exercise the option, so it remains unexercised and the investor sells the underlying asset for 60 in the spot market. Its profit* equals the gain on the sale of the underlying asset minus the premium paid = (60 - 50) - 5 = 5

So, if the price moves up or down equally, the seller of the underlying gets the same result thank to buying a put option.

* Profit excluding time value of money

Options on Moscow Exchange

Two types of options with different features are traded on the Moscow Exchange Derivatives Market. They are American future-styles deliverable and European equity-style cash-settled options.

Comparative overview – Moscow Exchange options

To find out more about the stock options, see the FAQ on single stock options.